🐍 Options models are wrong

Length: • 5 mins

Annotated by John Shelburne

John Shelburne: Q: Treat me as if I am an eight-year-old asking this question: What does implied volatility mean? A: Implied volatility is a number that tells you how jumpy people think something will be in the future — bigger number means they expect bigger up-and-down moves — and we get that number by looking at how much people are willing to pay for a safety ticket (an option) that protects against those moves. Market Syntax Implied volatility is the percentage the market is willing to pay for an option that reflects how big a price swing people expect for the underlying asset over the option’s life — higher implied volatility means traders expect larger moves. It’s not a direct prediction but a number backed out from the option’s market price that summarizes collective expectations and demand for protection. It is the single number you back out from a price for a time-limited right that summarizes how big future swings people are pricing in for that right; it’s the volatility input which, when put into the pricing formula, reproduces the observed price and thus encodes collective expectations about future variability. Q: I want a simple, easy-to-understand explanation of the term "surface". What is that? A: A "surface" is just a table of numbers you can picture as a smooth sheet — here it’s implied volatility arranged by strike (side-to-side) and time to expiration (front-to-back), so you can see how volatility changes across strikes and maturities in one view. In options, a "surface" (specifically an implied volatility surface) is a 2‑D grid of implied volatilities organized by strike (or moneyness) on one axis and time to expiration on the other, representing how market-implied volatility varies across strikes and maturities; it’s the structured object you get after reshaping option-chain quotes into strike-by-maturity form for analysis and plotting.

Build an implied volatility surface with free data from Yahoo Finance and Python

Each week, I send out one Python tutorial to help you get started with algorithmic trading, market data analysis, and quant finance. Upgrade to a paid plan to access the code notebooks.

In today’s post, you’ll pull live options chains, inspect skew and term structure, and plot a 3D implied volatility surface.

What an implied volatility surface is

An implied volatility surface is a grid of implied volatilities across strike prices and expirations, built from market option prices.

The idea became mainstream after the 1987 crash made it obvious that constant-volatility models miss real pricing patterns. As equity index options matured in the 1990s, desks started treating skew and term structure as first-class inputs, not chart curiosities.

How pros use it

That history shows up directly in modern workflows, because volatility surfaces sit between raw option quotes and real pricing decisions.

On a derivatives desk, you’ll usually start by pulling the full option chain, filtering obvious quote issues, and organizing it into strike-by-maturity form so you can see structure quickly. Risk teams use the same surface view to sanity check model marks and explain why a book’s sensitivity changes when the skew shifts. Systematic shops also use surface features as data inputs, for example tracking how short-dated implied volatility moves relative to longer maturities around macro events.

Why it’s worth learning

Once you can build a surface, you stop treating options data as disconnected rows and start treating it as a coherent object you can test.

You’ll also make fewer beginner mistakes like comparing implied volatility across expirations without aligning strikes, or plotting noisy points without realizing you need filtering and reshaping first.

Let’s see how it works with Python.

Library installation

Install the third-party libraries used to pull option chains and plot the volatility surface so the notebook runs end-to-end on a fresh environment.

If you are running in a locked-down environment (some corporate JupyterHub setups), you may need to ask for yfinance to be whitelisted or installed via your platform’s package manager instead of pip.

Imports and setup

We use datetime for “days to expiration,” pandas for reshaping the option chain into a grid, numpy for meshing coordinates for 3D plotting, matplotlib for charts, and yfinance to fetch live option chains from Yahoo Finance.

Pull every listed expiration for a ticker and standardize the result into one DataFrame so we can later compare strikes and maturities as a single surface instead of isolated rows.

This “one table” shape is the bridge from raw quotes to analysis: once the chain is consolidated, we can slice skew, slice term structure, and then reshape into a strike-by-maturity grid. Adding a consistent expiration timestamp also avoids subtle grouping bugs when expirations come in as strings.

Pull options chain across expirations

Fetch SPY’s full option chain and isolate calls so our first surface focuses on one option type with a cleaner skew signal.

Working with a liquid ETF like “SPY” helps because you typically get enough strikes and expirations to see real structure rather than sparse, jumpy points. Splitting calls and puts early is also practical because the skew often differs by type due to supply/demand and moneyness conventions.

Quickly list expirations available in the downloaded data so we know what maturities we can build the grid from.

This check is a small but useful workflow habit: when beginners think “the data is wrong,” it’s often just that the expiry set changed or a filter removed most rows. Seeing the available expirations keeps our later slices and plots grounded in what we actually pulled.

Slice skew and term structure

Take one expiration to study skew across strikes, and take one strike to study the term structure across expirations, filtering out near-zero implied vols that are usually stale or broken quotes.

These two “1D cuts” are the simplest way to stop thinking in single-vol terms: skew tells us how vol changes with strike, and term structure tells us how vol changes with maturity. The small impliedVolatility filter is not cosmetic; it prevents a few bad points from dominating the chart and misleading our interpretation.

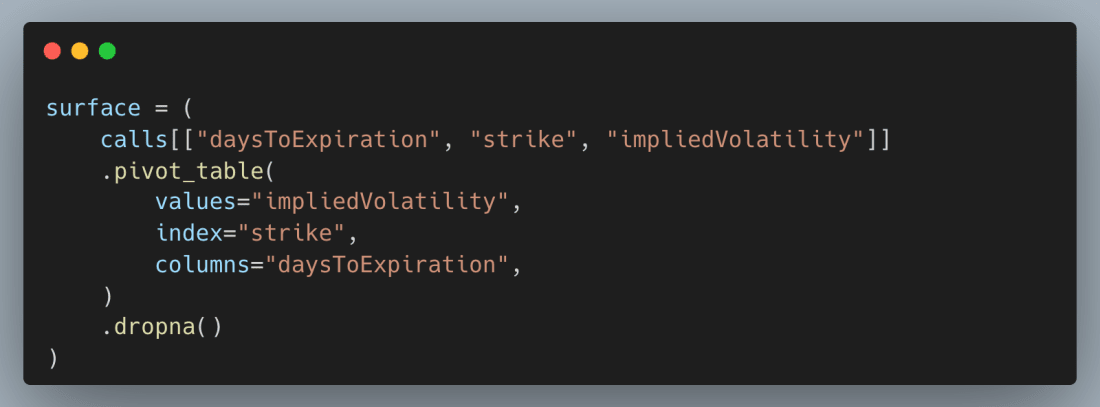

Reshape call implied vols into a strike (rows) by days-to-expiration (columns) grid, which is the core object we need for a clean surface plot.

Pivoting is the “professional workflow” step in this post: it turns a long options table into a coherent surface you can sanity check, model, and compare over time. Dropping NaNs is a pragmatic way to get a rectangular grid for plotting, but it also teaches an important lesson that real option chains are incomplete, so filtering choices shape what you see.

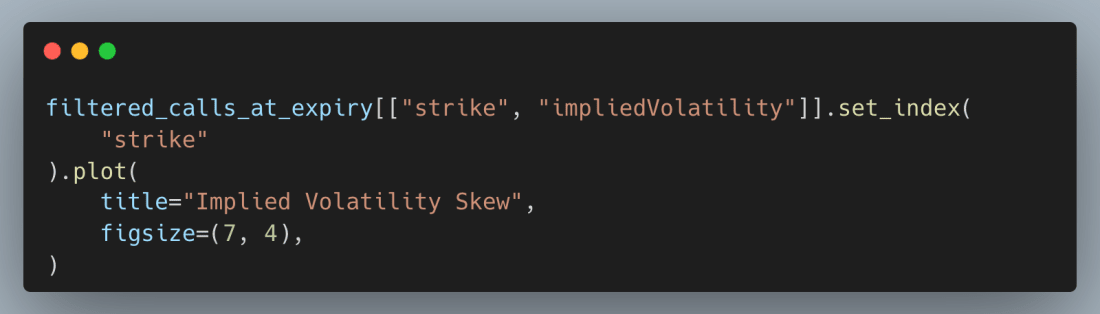

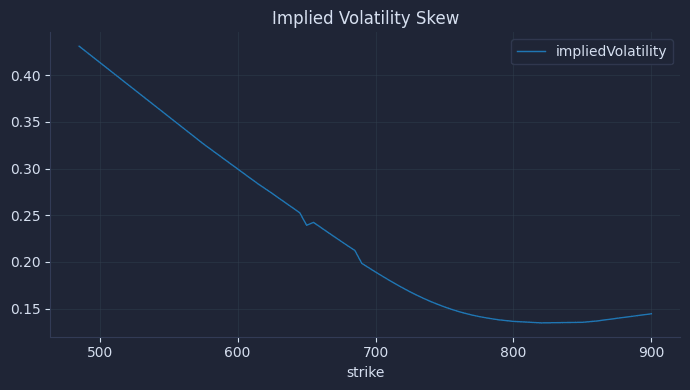

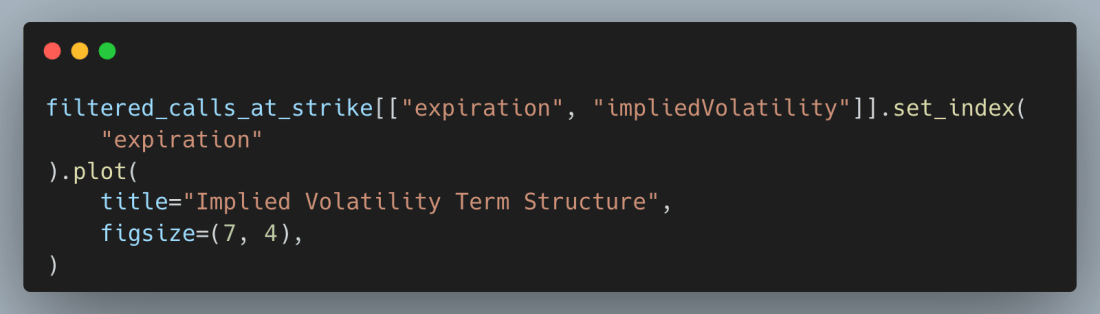

Plot the skew at a fixed expiration and the term structure at a fixed strike so we can visually confirm structure before moving to 3D.

The result is a volatility skew chart.

And the term structure.

Here’s the chart.

These plots act like unit tests for our surface: if skew and term structure look unreasonable, it’s better to debug filters and data alignment here than after a 3D plot hides the issue. In practice, desks will check these slices routinely because they map directly to common risk narratives like “skew steepened” or “front vol jumped.”

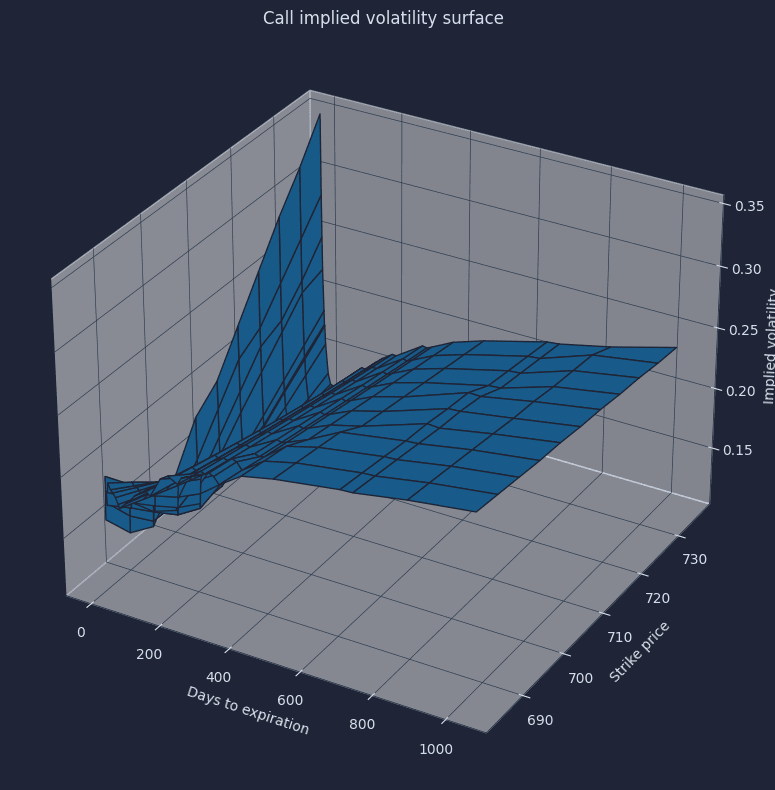

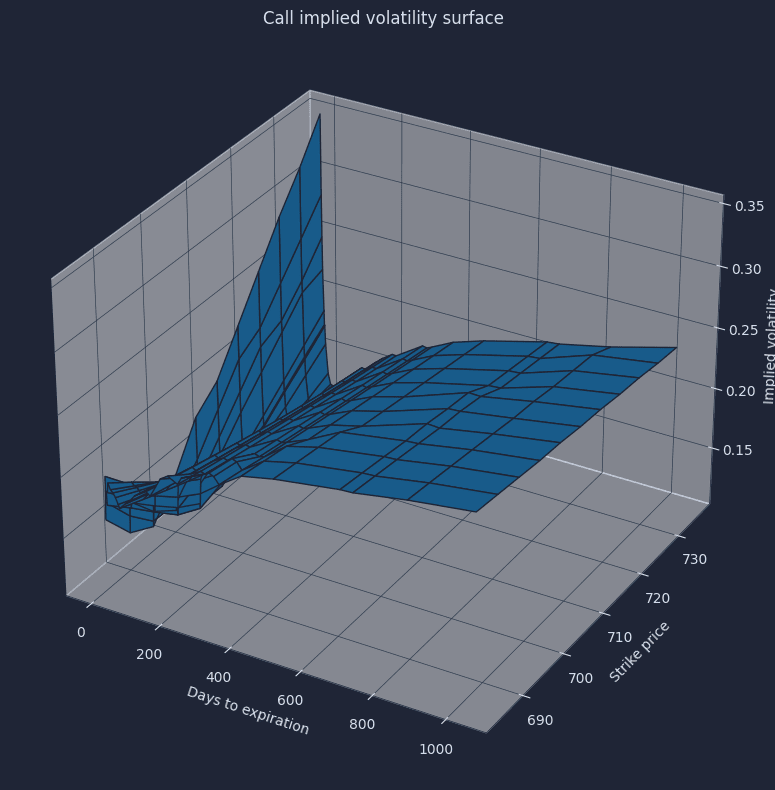

Plot the full implied vol surface

Build a 3D surface plot from the grid so we can see skew and term structure together as one object rather than flipping between expirations by hand.

The result is a plot that looks like this.

The surface is the payoff: it makes market structure obvious and helps us avoid false “bad data” hunts when the shape is actually real pricing information. Once we have this, we can start asking better questions, like which region of the surface moved after an event or whether our hedges are sensitive to skew versus overall vol level.

Your next steps

You can now pull a live options chain, reshape it into a strike-by-maturity grid, and plot a clean 3D implied volatility surface so skew and term structure are obvious. In practice, that surface is the quickest way to separate market structure from quote noise and to explain pricing and hedge behavior without relying on a single “one-number” vol.

Never investment advice. Use at your own risk. For educational purposes.

Upgrade for direct access to Priority Chat for personalized support plus updated tutorials that keep your Python code working as libraries evolve.