FFTT Full Report November 28, 2023

Length: • 12 mins

Annotated by Pat

Fed just touched off 3rd instance of UST market dysfunction in past 13 months; USD liquidity cometh.

– FFTT, 10/17/23

Last time the “Soros Imperial Dollar Cycle” drove the USD up and the US Insolvency Ratio as high as it is now, the USD was weakened significantly a short time later.

– FFTT, 10/31/23

Given the choice of “hurt the UST market and real economy” or “weaken the USD”, these three Treasury TBAC reports strongly suggest Treasury just chose “weaken the USD.”

– FFTT, 11/7/23

Exceedingly weak 30y UST auction suggests a much weaker USD will likely be pursued soon

– FFTT, 11/14/23

DXY breaks below the 200-day MA; let the games begin!

-Steph Pomboy, via X, 11/21/23

Key points:

- Market action and events in the lead-up to and aftermath of recent US/China meetings in San Francisco suggest the possibility that a deal to weaken the USD v. CNY was reached (even if only temporarily.) In this report, we weigh numerous pieces of evidence of such a deal.

- Our hypothesis of the rough structure of a potential “San Francisco Accord”:

- The US Treasury weakens the USD.

- China gets to buy oil in CNY from Saudi, etc. so the weaker USD does not hurt China’s current account via higher oil prices, which as we saw in August-September would force even more Chinese UST selling (thus reducing strain on UST markets.)

- China does not allow Saudi to recycle CNY into Chinese Government Bonds (CGB’s), but rather, into Chinese goods and gold.

- China stops selling USTs, and once the CNY rises v. USD, China resumes buying some USTs to help stabilize the UST market, and by extension, US asset prices, the US fiscal situation and economy (aiding demand for Chinese goods.)

*****

Ahead of the US/China meeting between Biden and Xi in San Francisco, the stronger USD and higher oil prices were threatening to push both the CNY and the all-critical UST market into severe crises, and with them, the global economy and monetary system.

Bob Elliott summarized the challenges China was facing as of October 23, 2023, as they were manifesting in the CNY...

...while FFTT has been highlighting how the stronger USD (especially when combined with higher oil prices) was creating a procyclical debt spiral in the all-important UST market in the 10/3/23 edition, the 10/17/23 edition, the 10/31/23 edition, the 11/7/23 edition, and the 11/14/23 edition of FFTT.

While the US and China are engaged in an increasingly tense economic and geopolitical competition, in our view, it is in no one’s interest for the existing monetary system to collapse chaotically, which was increasingly becoming an acute threat given market action in 3q23 (a nonlinear decline in CNY and nonlinear rise in 10y UST yields were threatening.)

Morbidly (but rationally), it seems the US and China would rather compete against each other aggressively over the long term than cause the near-instant collapse of both of each other’s economies in what would amount to a spectacular but ultimately self-defeating (and foolish) demonstration of economic MAD (Mutually Assured Destruction.)

We believe that the acute strains in the CNY market and the UST market may have served to properly motivate both China and the US to agree to a deal to weaken the USD to buy time as Biden and Xi met two weeks ago in San Francisco:

Xi, Biden at APEC summit: China, US leaders meet in San Francisco – 11/15/23

Xi, Biden at APEC summit: China, U.S. leaders meet in San Francisco (cnbc.com)

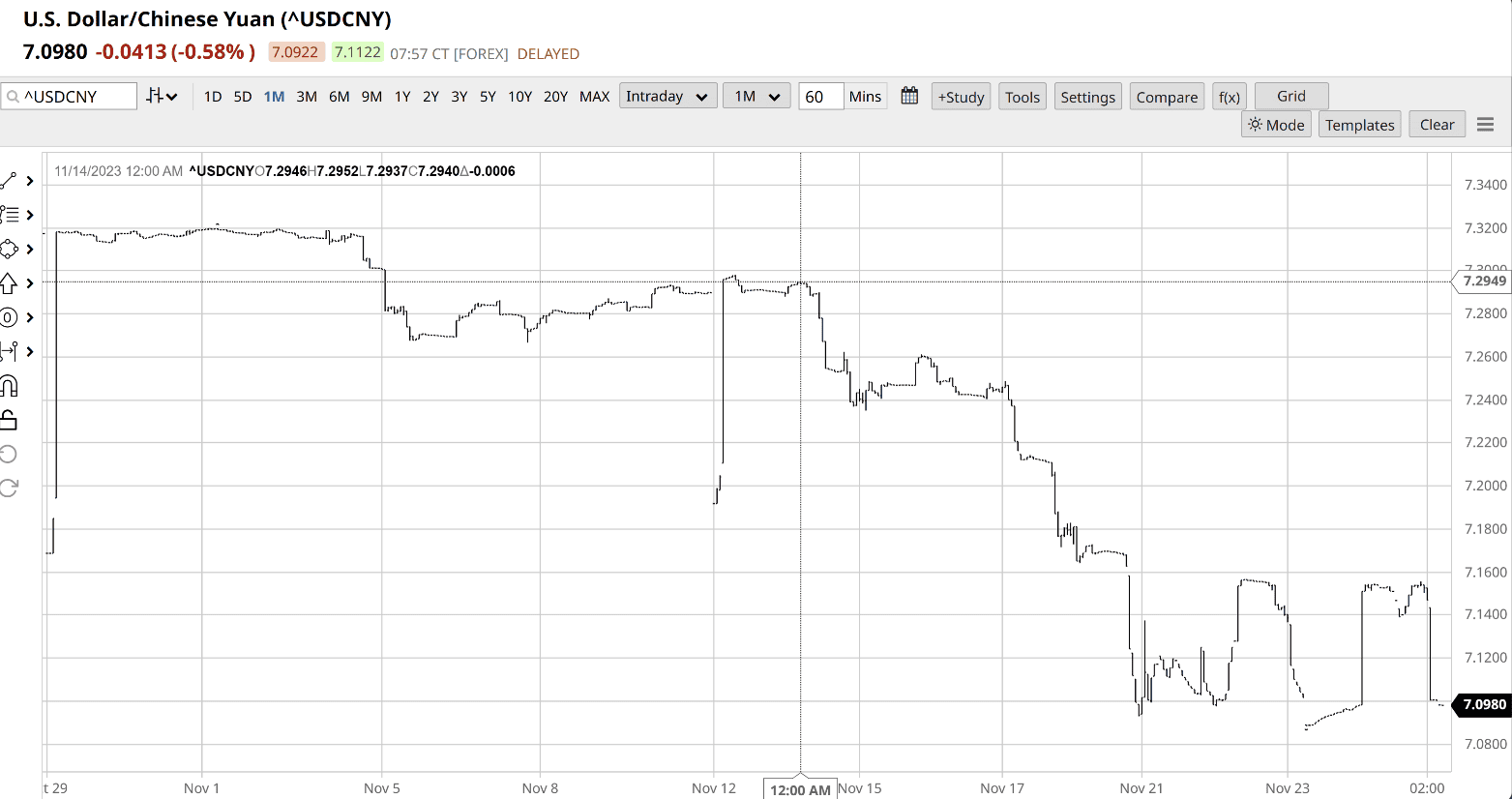

Beginning on November 14 (the day before Biden and Xi officially met), CNY/USD began rising sharply...

Source: Barchart.com

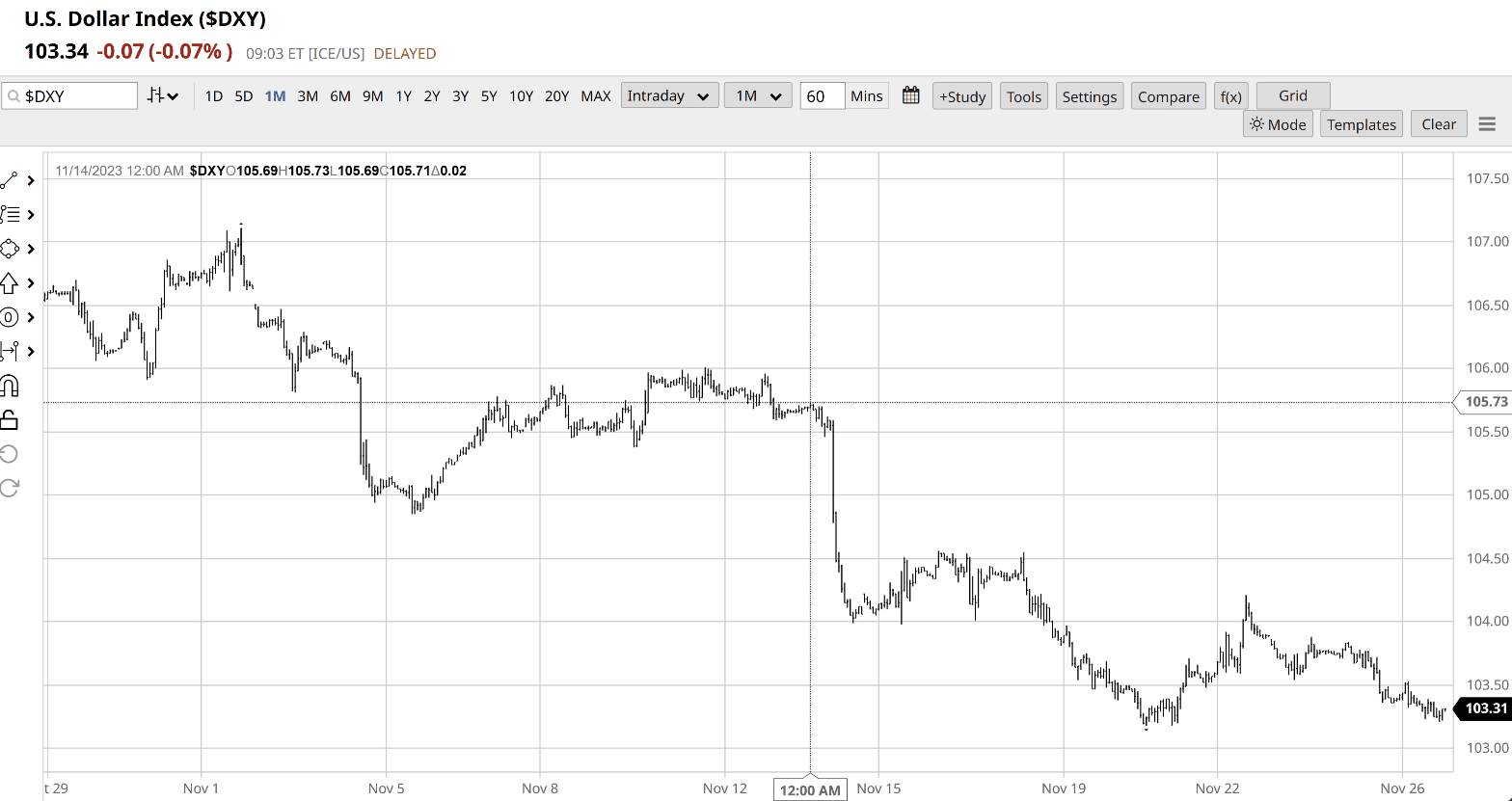

...and DXY began falling sharply (essentially USD v. EUR and JPY):

Source: Barchart.com

Nominally, the move down in the USD beginning on November 14 can easily be explained away – that was the day of the weaker-than-expected US CPI report, which occurred into a consensus position that was clearly positioned for continued “Higher for Longer” (given the reaction in markets)...as long as we assume that the US or any other country would never report an important data point with a policy goal in mind (weaker CPI would have weakened USD, and it did):

Markets News November 14, 2023: Nasdaq surges to 3-month high, bond yields sink on easing inflation – 11/15/23

Markets News, Nov. 14, 2023: Nasdaq Surges to 3-Month High, Bond Yields Sink on Easing Inflation (investopedia.com)

Stocks soared and Treasury yields fell Tuesday after data showed inflation slowed more than expected in October, raising hopes the Federal Reserve could be done with interest rate hikes.

The Nasdaq jumped nearly 2.4%, its biggest one-day gain since April, while the S&P 500 surged 1.9% and the Dow Jones Industrial Average rose 1.4%.

The yield on 10-year Treasurys fell nearly 20 basis points to their lowest in a month and a half. The yield on shorter-dated bonds fell even more dramatically.

Inflation decelerated to a standstill in October, a bigger slowdown than economists were expecting. Core inflation, which excludes volatile food and energy prices, unexpectedly slowed to 0.2% from 0.3% in September.

US CPI October 2023: Inflation broadly slows in sign of progress for Fed – 11/15/23

US CPI October 2023: Inflation Broadly Slows in Sign of Progress for Fed – Bloomberg

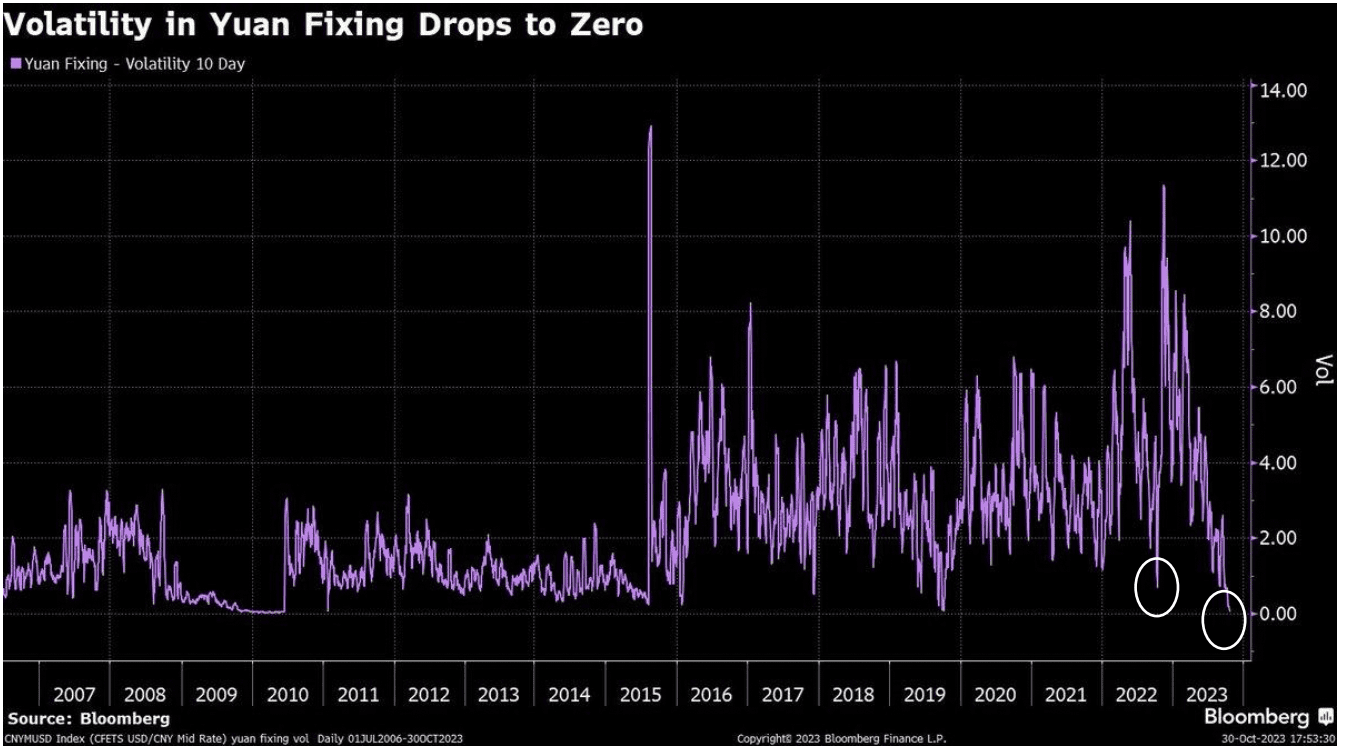

Here’s the thing though: The “weaker inflation drove the USD lower” does not explain the collapse in CNY fix volatility by the most since October 2022, which occurred in late October! (white circles below) Critically, the last time CNY fix volatility was this low was shortly before Treasury Secretary Yellen attended an IMF meeting in Washington DC that saw US allies complain about USD strength and the USD weaken notably over the ensuing four months (h/t DC) as Yellen rapidly ran down the Treasury General Account (TGA):

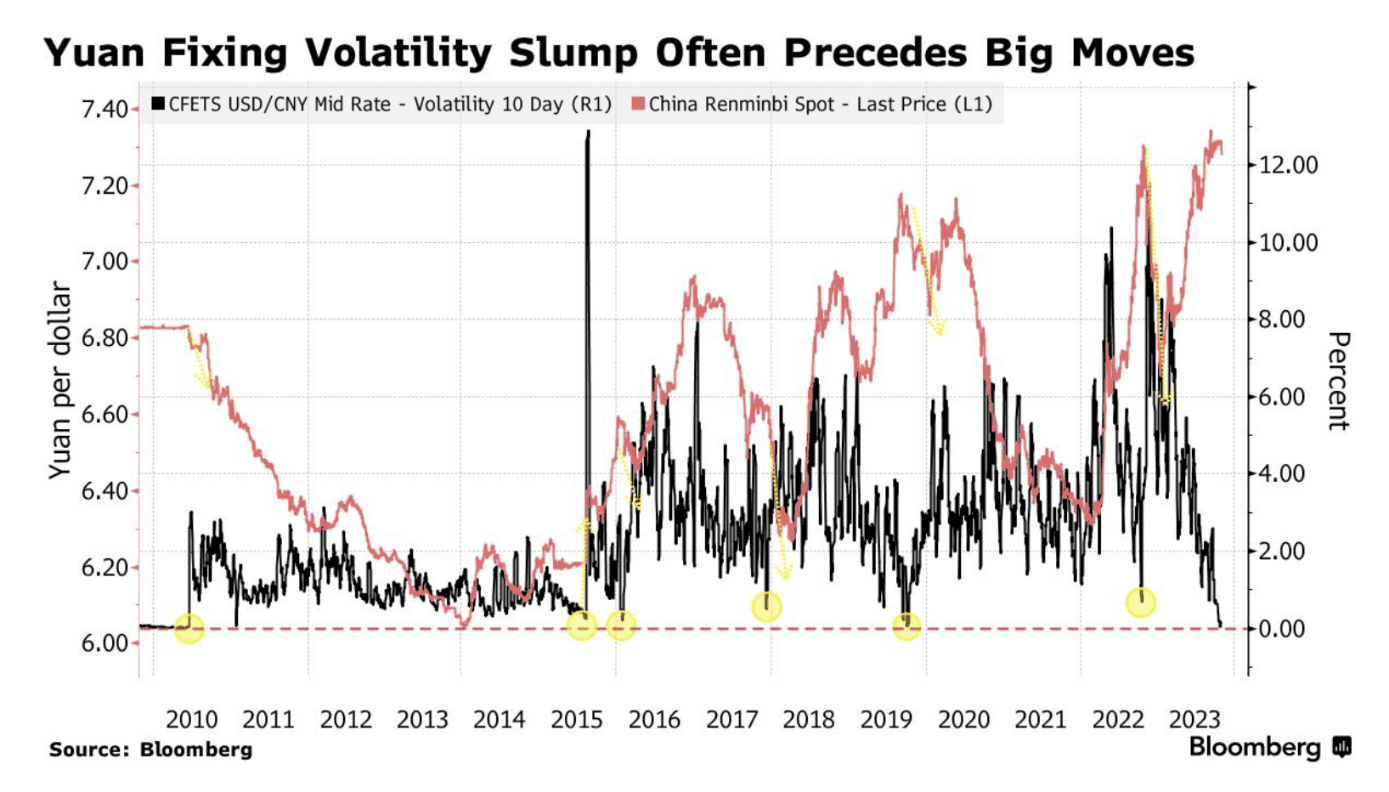

Equally critically, prior collapses in CNY fixing volatility in late 2015, late 2017, 3q19, and 3q22 (per above) presaged pronounced CNY strength and USD weakness (yellow circles below):

Adding to our “Spidey sense” that some sort of agreement on the USD had been reached by China and the US in San Francisco was this announcement, made just five days after the meeting:

China, Saudi Arabia sign currency swap agreement – 11/20/23

China, Saudi Arabia sign currency swap agreement | Reuters

Recall that last December, Xi called for oil trade in CNY at his Gulf summit with Saudi’s MBS in Riyadh:

China’s Xi calls for oil trade in CNY at Gulf summit in Riyadh – 12/10/22

China’s Xi calls for oil trade in yuan at Gulf summit in Riyadh | Reuters

Also recall that in August, Saudi, UAE and Iran were invited to join the BRICS at the annual BRICS Summit:

Saudi Arabia, UAE, and Iran among six countries invited to join BRICS – 8/24/23

BRICS: Saudi Arabia, UAE and Iran among six countries invited to join group | CNN Business

All of the preceding headlines make the news that Saudi’s trade surplus with China exploded higher in the month immediately after the BRICS Summit (September) even more interesting:

Saudi Arabia’s trade surplus with China soars by 257% in September – 11/27/23 (via MH, GT)

Saudi Arabia’s trade surplus with China soars by 257% in September (arabnews.com)

The trade surplus with China soared to SR6.67 billion ($1.78 billion), reflecting a 257 percent surge compared to August.

During this period, Saudi Arabia recorded an increase in exports to China at a growth rate of 34 percent reaching a total of SR18.99 billion. Exports comprised mainly oil, to which this increase is attributed, and non-oil products included chemical components, plastic, and rubber.

China’s share of Saudi Arabia’s exports also saw a rise from 14 percent in August to 18 percent in September.

Adding to the intrigue, further note that China and the UAE just renewed their currency swap deal today:

UAE Central Bank renews $4.9 billion currency swap deal with China – 11/28/23

UAE Central Bank renews $4.9bn currency swap deal with China (thenationalnews.com)

All of which carries even more weight in our view when married with this headline from this week, showing bullion bank Standard Chartered offering exchange services for digital CNY (which would theoretically facilitate all of what we just described – CNY trade of energy, outside the USD system “pipes”, net settled in physical gold)...

STANDARD CHARTERED CHINA OFFERING EXCHANGE SERVICES FOR DIGITAL YUAN – COINDESK – 11/27/23

...especially considering that Standard Chartered trades gold and commodities “in more jurisdictions globally than any other bank in the world”, including in several major CNY and gold trading hubs (Shanghai, HK, Singapore, London):

We have [commodity] trading centres across the world – in Shanghai, Hong Kong, Singapore, London, and New York. And no other bank trades in as many jurisdictions globally. This means as well as giving unrivalled access to on-the-ground market news, we can provide a follow-the-sun model for all your hedging and yield-seeking needs.

When we put all of the preceding facts together and let them “marinate in our brain” for a bit, here’s what we think the deal is:

The US weakens the USD; China gets to move ahead full-steam with buying energy and commodities in CNY, facilitated by the rollout of the digital CNY, which will serve to weaken the USD notably over time. There are likely two additional key conditions attached to this, in our view:

- Saudi and other oil producers are NOT allowed to recycle CNY surpluses into Chinese government bonds (CGB’s), which the US would likely see as a red line as it would amount to OPEC+ financing the Chinese military...but OPEC+ would be free to recycle CNY surpluses into Chinese goods and any net surpluses into gold, which should be very good for gold over time.

- Once the USD weakens enough, China stops selling USTs and instead buys some USTs to support UST markets and therefore the US fiscal situation and the US economy, which remains a major end market for China.

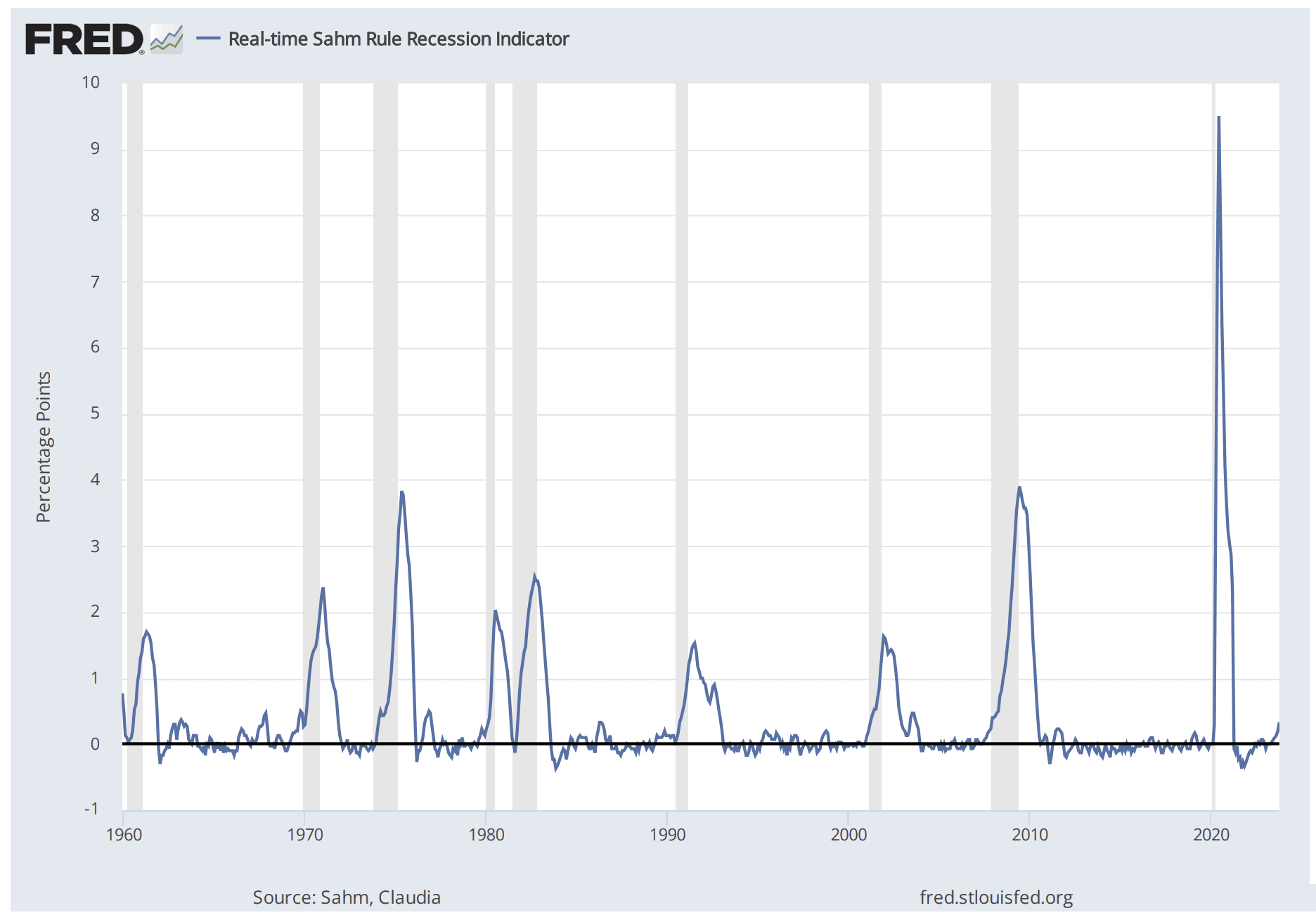

All of this raises the question, why now? Reason #1: The US may already be in a recession...

America may soon be in recession, according to a famous rule – 11/14/23

America may soon be in recession, according to a famous rule (economist.com)

For financial markets the Holy Grail is a perfect leading indicator—a gauge that is both simple to monitor and consistently accurate in foretelling the future. In reality, such predictive perfection is unattainable. It is often hard enough to grasp what is happening in the present, let alone the future. A perfect real-time indicator would thus be a potent goblet of knowledge, if not quite the Holy Grail, for investors and analysts to drink from. Recently they have turned their attention towards one impressive candidate: the Sahm rule.

Developed by Claudia Sahm, a former economist at the Federal Reserve, in 2019, the rule would have been capable of identifying every recession since 1960 in its early stages, with no false positives. This is no mean feat given that the body which officially declares whether the American economy is in recession sometimes needs a full year of data. The Sahm rule, by contrast, typically needs just a few months.

Here’s the St. Louis Fed’s description of “The Sahm Rule”:

Sahm Recession Indicator signals the start of a recession when the three-month moving average of the national unemployment rate (U3) rises by 0.50 percentage points or more relative to the minimum of the three-month averages from the previous 12 months.

This indicator is based on “real-time” data, that is, the unemployment rate (and the recent history of unemployment rates) that were available in a given month. The BLS revises the unemployment rate each year at the beginning of January, when the December unemployment rate for the prior year is published. Revisions to the seasonal factors can affect estimates in recent years. Otherwise the unemployment rate does not revise.

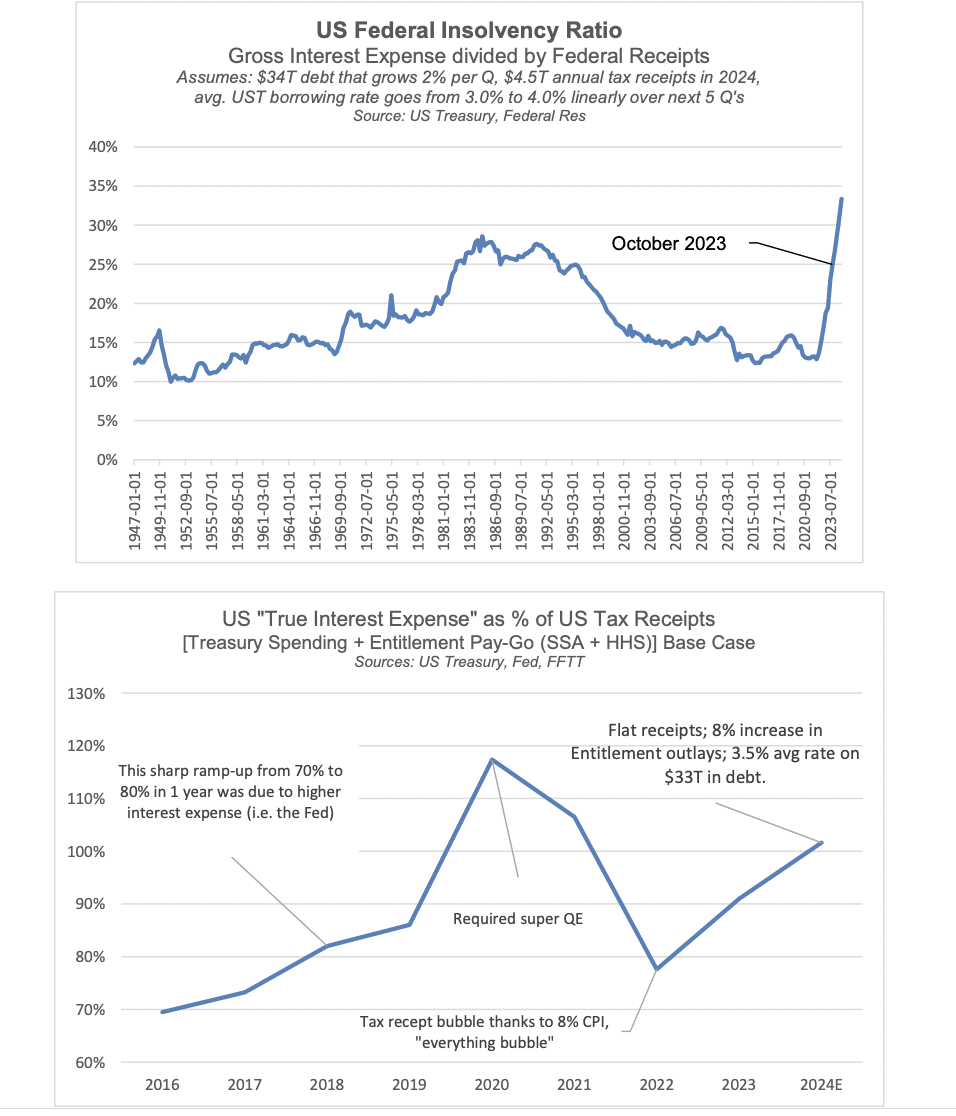

This in turn is important because as we have been highlighting ad nauseum for the past 3+ months, a recession is NOT a policy option with the US insolvency ratio where it is (first chart) and US “True Interest Expense” about to go back >100% of US Federal receipts – in all prior instances of the insolvency ratio and True Interest Expense being this high, the USD was weakened significantly and immediately; a MUCH weaker USD is required, ASAP.

This brings us to Reason #2 for “why weaken the USD now?” – this reason is more strategic: As we have repeatedly shown, the US defense industrial base has been severely weakened by offshoring (especially to China) to the point of being a national security risk, but the US cannot re-shore its defense industrial base unless the USD is weakened MEANINGFULLY.

This in turn makes the following headline from yesterday even more potentially interesting:

Biden will convene his new supply chain council and announce 30 steps to strengthen US logistics – 11/27/23

Biden will convene his new supply chain council and announce 30 steps to strengthen U.S. logistics (cnbc.com)

President Joe Biden on Monday will convene the first meeting of his supply chain resilience council, using the event to announce 30 actions to improve access to medicine and needed economic data and other programs tied to the production and shipment of goods.

“We’re determined to keep working to bring down prices for American consumers and ensure the resilience of our supply chains for the future,” said Lael Brainard, director of the White House National Economic Council and a co-chair of the new supply chain council.

The announcement comes after supply chain problems fueled higher inflation as the United States recovered from the coronavirus pandemic in 2021. While consumer prices are down from last year’s peaks, polling shows that inflation remains a political challenge for Biden going into the 2024 presidential election.

Among the 30 new actions, Biden, a Democrat, will use the Defense Production Act to have the Health and Human Services Department invest in the domestic manufacturing of needed medicines that are deemed crucial for national security.

While we are not lawyers (so take this with a block of salt and please do your own due diligence with any Washington DC consultants you have relationships with), we studied the Defense Production Act provisions a bit when Trump cited it early in his term, and our understanding at the time was that it offers the President wide latitude to pursue action without a lot of interference from Congress.

*** SO HOW DO WE MAKE MONEY WITH THIS? ***

To sum it up: We appear to have means, motive, opportunity, and price action all supportive of a potential deal to weaken the USD being struck between the US and China in San Francisco two weeks ago.

What are we watching in the meantime to gauge whether we are right? DXY, CNY/USD, both gold and the gold/oil ratio:

- Gold and the Gold/Oil ratio should continue rising over time, regardless of real rates.

- DXY should continue falling.

- CNY should continue rising v. USD.

If we are right, this should stabilize the UST market (yields), all of which should be positive for US and global equities. Inflation should stabilize for a few months and then begin to re-accelerate.

If we are wrong, the US fiscal position which is already in acute distress will likely deteriorate nonlinearly as the US heads into a recession, sending us right back to the worst parts of August-September 2023: USD likely spikes higher, UST yields likely rise, UST auction sloppiness likely returns and gets worse, global risk-off, oil down, and likely gold and BTC up (as the only counterparty risk-free collateral in the system.)

In other words, if we are wrong about there being an agreed-to deal between the US and China to weaken the USD, we will likely move toward the Mother of All Crises.

It is critical to understand that even if we are right, weakening the USD will only buy some time – 3-6 months, maybe even up to a year, as US and global economic activity should bounce back sharply with a weaker USD, as should global asset prices. This would in turn serve to significantly increase US tax receipts (i.e., reduce UST issuance needed), which should stabilize bond markets and therefore risk assets...but only until inflation picks back up.

We estimate the gap between “weaker USD is good” to “weaker USD is driving growth and inflation back up, so it is bad again” as being 3-6 months, maybe up to a year...but that is nothing more than a wild-a$$ guess, offered to frame how we are thinking about the aforementioned dynamic at the moment.

We are not changing positioning, other than continuing to add to our already oversized gold and BTC positions on any weakness, out of our (still large but smaller in recent weeks) cash position.

Thank you for reading this edition of FFTT. LG

© Copyright 2023, FFTT LLC.

DISCLOSURES:

FFTT, LLC (“FFTT”), is an independent research firm. FFTT’s reports are based upon information gathered from various sources believed to be reliable but are not guaranteed as to accuracy or completeness. The analysis or recommendations contained in the reports, if any, represent the true opinions of the author. The views expressed in the reports are not knowingly false and do not omit material facts that would make them misleading. No part of the author’s compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views about any and all of the subject securities or issuers. However, there are risks in investing. Any individual report is not all-inclusive and does not contain all of the information that you may desire in making an investment decision. You must conduct and rely on your own evaluation of any potential investment and the terms of its offering, including the merits and risks involved in making a decision to invest.

The information in this report is not intended to be, and shall not constitute, an offer to sell or a solicitation of an offer to buy any security or investment product or service. The information in this report is subject to change without notice, and FFTT assumes no responsibility to update the information contained in this report. The publisher and/or its individual officers, employees, or members of their families might, from time to time, have a position in the securities mentioned and may purchase or sell these securities in the future. The publisher and/or its individual officers, employees, or members of their families might, from time to time, have financial interests with affiliates of companies whose securities have been discussed in this publication.