And how will this affect startups and the financial system?

The big news in both the tech and financial worlds right now is the run on Silicon Valley Bank. SVB, as it’s known, was a bank that lent a lot of money to startups (or “startups”, i.e. bigger tech companies that are still private), and provided a lot of financial services to both startups and other tech companies. Here’s a good rundown of what it did.

I use the past tense, though, because on Thursday (i.e. yesterday), a bunch of people pulled their money out of the bank. The bank didn’t have enough cash to pay out all the people who were asking for their money back, so it collapsed. The FDIC, the government agency responsible for preventing and cleaning up bank failures, took the bank into receivership.

What does that mean? First, SVB was an FDIC insured bank, meaning that up to $250,000 of every insured depository account (checking account, etc.) in the bank is safe. If you have $250,000 or less in an SVB account, it’s no problem — the government will pay you your cash. The problem here is that most of the deposits in SVB — 93%, by most reports — were not FDIC insured, because they were over the $250,000 limit. These deposits will be partially paid off by the FDIC, which will sell SVB’s assets and pay deposit-holders an “advanced dividend” sometime in the next week.

So let’s talk a bit about why this happened, and what the ramifications will be.

This was a very normal bank run on a very unusual bank

First, let’s review the basics of bank runs. (If you know this stuff you can skip to the next section.)

Fundamentally, a bank is a company that borrows short and lends long. Checking accounts, for example, represent money that a bank borrows from depositors. The bank has to pay that money back to depositors whenever they want it — if you go to an ATM or a bank window and withdraw your money, you get it instantly. Banks don’t pay very high interest on checking accounts or their other short-term liabilities. Meanwhile, the bank invests in long-term assets — mortgages, for example, or corporate loans — that earn a high return, but can’t be quickly liquidated (or at least, not for full value).

The difference between the high return on their long-term assets and the low cost of their short-term liabilities is called the interest rate spread, and it’s the most important way that banks make their profits. But this is a risky business. Because the assets are illiquid long-term stuff, they can’t quickly be sold off for full value. So if all the people who lend money to the bank (e.g. depositors) come asking for their money back all at once, the bank simply won’t be able to pay them all off. This risk is called maturity mismatch. And when the lenders all ask for their money back at once, it’s called a bank run.

Back in the financial crisis of 2008, there were a lot of very complicated crises and collapses that were sort of like bank runs, which happened to companies and other entities that were sort of like banks. Economists spent years modifying their traditional models of bank runs to try to describe these weird events. But in the case of Silicon Valley Bank, the run was a completely normal, classic bank run, of the type that’s depicted in movies like Mary Poppins and It’s a Wonderful Life. Economists understand this kind of run very well — in fact, just this past year, Douglas Diamond and Philip Dybvig won a Nobel prize for making a model of it.

The key to a classic bank run is called sequential service. Basically, in a classic run, whoever tries to take their money out of a bank first will be able to get all of it out, while the latecomers will lose their money when the bank fails. This means that runs are self-fulfilling prophecies — as soon as a critical mass of people all believe a bank is likely to suffer a run, they all stampede to pull their money out at once in an attempt to get in ahead of everyone else. And this stampede is the run.

Normally FDIC insurance stops this kind of run from happening. Because everyone knows the federal government will cover their deposits, they aren’t worried about losing their money in a run, so they’re never in a rush to pull it out. And because they never rush to pull it out, runs can’t even get started. For a normal bank, about 50% of deposits are FDIC insured

But 93% of SVB’s deposits were not FDIC insured. So SVB was vulnerable to a classic, textbook bank run.

Why did SVB have so many uninsured deposits? Because most of its deposits were from startups. Startups don’t typically have a lot of revenue — they pay their employees and pay other bills out of the cash they raise by selling equity to VCs. And in the meantime, while they’re waiting to use that cash, they have to stick it somewhere. And many of them stuck it in accounts at Silicon Valley Bank.

If you’re a startup founder, why would you stash your cash in a small, weird bank like SVB instead of a big safe bank like JP Morgan Chase, or in T-bills? This is actually the biggest mystery of this whole situation. Some companies put their money in SVB because they also borrowed money from SVB, and keeping their money in SVB was a condition of their loan! For others, it was a matter of convenience, since SVB also provided various financial services to the founders themselves. For yet others, it might have just been vibes and hype — maybe you used SVB because you’re a startup, and that’s just the bank that startups use, duh! And also groupthink — about half of all startups used SVB, according to some reports, so maybe people put their money there because their friends and acquaintances did too.

But anyway, taking giant deposits from startup companies instead of individuals and small businesses made SVB a very weird bank, which made it vulnerable to a run.

What started the run?

The next question is what started the run on SVB. There are basically three possibilities here:

a self-fulfilling prophecy,

worries about the value of SVB’s assets, and

withdrawals due to a worsening VC investment situation.

Let’s start with the self-fulfilling prophecy. Technically, you don’t need any real fundamental reason for a bank run to get started — all you need is for a critical mass of people to worry that a critical mass of people is about to pull their money out. The SVB run started when Peter Thiel’s VC firm, Founders’ Fund, advised its portfolio companies to pull their money out of SVB. Matt Levine suggests that because startups tend to follow the pronouncements of top VCs en masse, just one call like this can start a stampede:

Also, I am sorry to be rude, but...nobody on Earth is more of a herd animal than Silicon Valley venture capitalists...if all of your depositors are startups with the same handful of venture capitalists on their boards, and all those venture capitalists are competing with each other to Add Value and Be Influencers and Do The Current Thing by calling all their portfolio companies to say “hey, did you hear, everyone’s taking money out of Silicon Valley Bank, you should too,” then all of your depositors will take their money out at the same time.

So there are going to be some people who just blame Thiel and a couple other VCs for the run. And maybe they’re right — maybe Thiel was just spooked by the collapse of the crypto bank Silvergate a couple days ago, or maybe he had something against SVB, or maybe he just woke up in a poopy mood.

But I suspect it wasn’t just a random occurrence. I think Thiel and others were genuinely worried about the bank’s solvency.

A common trigger for a bank run is that people worry that the value of the bank’s assets has fallen below the level of its liabilities. Insolvency isn’t automatically the kiss of death for a bank — its assets could go back up and return it to solvency. But if you have some reason to believe that a bank is insolvent, then that makes you more likely to pull your money out, because it increases the chance that the bank won’t be around for long.

There are a number of reasons why the value of SVB’s assets fell. One is that interest rates have gone up a lot in recent months. SVB invested in a lot of fixed-rate bonds and loans, and when interest rates rise, the price of fixed-rate bonds and loans falls. Another is that there has been a gigantic crash in the tech world over the past year — itself partly due to a rise in interest rates but also to a localized bubble and to other longer-term factors. This means that lots of startups are probably headed for the scrap heap as soon as they run out of money, which makes them more likely to default on their SVB loans.

Fears that SVB was insolvent grew on Wednesday (March 8) when the bank declared a big writedown on its assets and announced a stock sale to raise capital. The writedown by itself wasn’t enough to make the bank insolvent, or close to it, but it probably spooked some people into thinking that even bigger writedowns were in the near future. Some people allege that SVB announced the stock sale in a clumsy way that created maximum fear:

SVB made the responsible decision to strengthen its financial position with a cap raise.

It made sense.

Where things went terribly wrong was the communication, specifically:

(1) WHAT they said, (2) WHO the audience was, (3) WHEN they did it, and (4) HOW they framed it.

In any case, the fear of big losses from rate hikes and the tech bust were probably a factor here.

And there might have been one more factor here. For normal banks in normal conditions, depositors withdraw their money from banks at pretty much random times. This means that statistically, net withdrawals in any given month or year are not likely to become big enough to cause problems. But since many of SVB’s depositors were tech startups, it was possible that their withdrawals were highly correlated even before the run began.

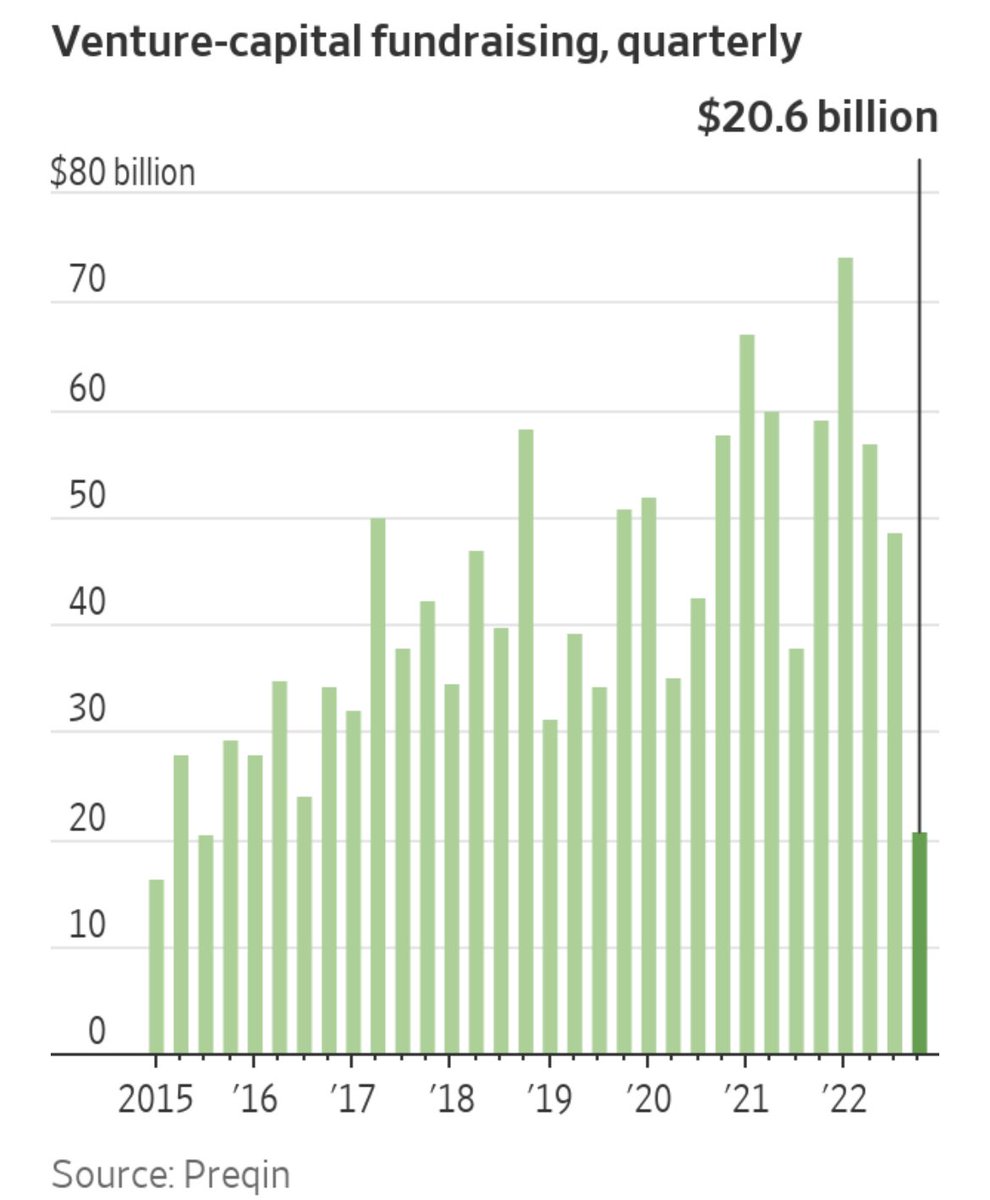

The obvious reason for a big wave of startup cash withdrawals would be the collapse in venture funding that has happened as a result of the recent tech bust:

VC firms raised $20.6bn Q4, a 65% drop from the year-earlier quarter and the lowest Q4 amount since 2013

LPs invested in 226 VC funds in Q4 2022 compared to 620 funds in Q4 2021

With VC funding having dried up, many startups had to survive by using their “runway” — burning through cash to pay their employees and other expenses while they waited for the market to recover. But this meant a lot of startups were all withdrawing a bunch of cash from SVB, while new VC rounds were failing to give SVB new deposits.

To meet these simultaneous demands for cash from startups using up their runway, SVB had to sell assets. Of course it sold its most liquid assets first, leaving it with a pile of assets that was much less liquid. That made it more vulnerable to a bank run. In addition, those sales of assets might have been the ones that spooked some depositors into thinking SVB was actually insolvent, which helped trigger the actual run.

In other words, SVB was just another casualty of the tech bust, and it went bust in the way that banks traditionally go bust.

What will be the effect on startups, tech, and the financial system?

Now let’s talk about what the effect of this bank failure will be.

The first question, which I’m sure will be foremost in the minds of startup founders and employees, is: How much of the money they had kept in SVB can startups expect to recover, and when?

On Monday, each SVB account holder will get $250,000 of their money back (or if they had less than $250k, they’ll get it all back). After that, the FDIC will attempt to sell off SVB’s illiquid assets, and it’ll use the cash to pay back as much of the uninsured deposits as it can.

Now, there are a couple of different ways that sale could go. We often think of a fire sale, where illiquid assets with uncertain fundamentals get sold off quickly for a fraction of their previous valuation. That is possible here. If that happens, companies who had unsecured deposits at SVB could lose some percent of those deposits.

That’s a worst-case scenario. But unlike in 2008, we’re not facing a situation where most big banks are collapsing at once — so far, at least, it’s just this one weird bank in an unusual corner of the economy. So it’s possible another big bank, like Goldman Sachs or JP Morgan Chase, could just buy most or all of SVB’s assets and take over its deposit accounts. Finding a single buyer would make the sale happen quickly, which would reduce the chance of panic and contagion, so I’m sure this is what the FDIC is trying to do now.

As for how much of a haircut depositors could take in a sale, this doesn’t seem like a situation where deposits are going to mostly vaporize. Some of SVB’s assets are startup loans, which might be hard to value, but nothing like the byzantine toxic housing assets involved in the 2008 crash. And a lot of SVB’s assets are just government bonds, which are very easy to value and which will have retained most of their value. So it’s very possible that even uninsured deposits will be made whole. Matt Levine thinks that the government will lean on SVB’s buyer(s) to make depositors whole, as a way of preventing panic and contagion:

I would also guess — not investing or banking advice! — that the [amount SVB’s assets get bought for] will...turn out to be higher than $188 billion [i.e. the amount of total deposits]...[I]t seems bad for the FDIC to wind up a big high-profile bank in a way that causes significant losses for depositors, including uninsured depositors...

If it turns out to be true that [SVB’s depositors] lose their deposits, there could be more bank runs...My assumption is that the FDIC, the Federal Reserve, and the banks who are looking at buying SVB all really don’t want that. If you are a bank looking at buying SVB, and you do a detailed analysis of its assets and conclude that they are worth $180 billion, and you come to the FDIC and say “I will take over this bank and pay the uninsured depositors 95 cents on the dollar,” the FDIC is going to look at you and say “don’t you mean 100 cents on the dollar,” and you are going to say “oh right yes of course, silly me, 100 cents on the dollar.”

The government occasionally lets banks collapse in a disorderly, disruptive way, out of a sense of wanting to ensure financial probity — the biggest example being the collapse of Lehman in 2008. But the recent experience in the pandemic suggests that the government has learned important lessons from 2008, and the need to prevent panic and contagion is a lot more important than the need to make a bunch of startups lose 5% or 20% of their cash as a punishment for putting their money in a weird risky bank.

The other big risk for startups — and the reason they’re currently panicking — is the possibility that they won’t be able to make payroll next week. But although this is undeniably scary, I doubt it’s a huge danger. First of all, lots of companies are small enough where they can get by for a week or two on $250,000. Second, the FDIC has promised to pay SVB’s depositors an “advance dividend” next week, which will also help make payroll. To do this, they’ll either A) find a buyer for all of SVB’s assets very soon, or B) sell off some of SVB’s more marketable bonds in order to send depositors enough cash to keep making payroll til they can complete the broader sale. The FDIC has a strong incentive not to let startups vaporize over the next few weeks because they can’t pay their employees. It’s going to be a nail-biting week or two for startups, but my advice is not to panic.

As for the employees, I doubt they will quit en masse, even in the worst-case scenario where they have to wait a week to get paid. Such are the risks of startup life. This also applies to the risk that payment processing companies will themselves go under, requiring startups to shift to new providers.

The longer-term effect of SVB’s collapse on the broader tech sector is likely to be negative, but not catastrophic. This episode and the general disruption and uncertainty it causes will add to the general air of pessimism that has prevailed since early 2022. SVB also provided a lot of other financial services to companies, and it will be annoying and dispiriting to have to find new providers. And SVB was itself an important tech investor, so its demise will exacerbate the overall startup funding crunch. In a way, this is just one more shoe dropping in the slow deflation of the Second Tech Boom. (On the bright side, more pessimism probably means higher returns for those who are both willing and able to invest while others are shunning the sector.)

Finally, let’s talk about the big risk: financial contagion. Many people will undoubtedly have traumatic memories of 2008, when Lehman’s collapse triggered a systemic meltdown. That is a real possibility, and it’s why the FDIC and other government agencies are probably going to work very hard to make sure SVB’s depositors don’t have to take haircuts.

But there are reasons this is not like the Lehman shock. First of all, in 2008 the big banks were all very exposed to each other — they had all lent each other money against the opaque, illiquid mortgage-backed assets that they had all created and sold to each other. This is just not the case with SVB at all — the financial system as a whole is just not particularly exposed to either SVB’s debt or the assets on SVB’s books. Bank stocks fell on the news about SVB, but this is probably just sentiment.

In general, I’m optimistic about the system’s ability to contain the fallout from SVB. So far the U.S. economy has powered along with record employment and strong growth, even as the tech sector has gone into a slump. There’s not a lot of reason to think that basic pattern will change after this bank run, and the government has every reason to make sure it doesn’t change.